Map of 110 Musical and Dramatic groups in Ireland. This captures about 25% of the total number of such groups.

Does it have to be “professional”

Much discussion of “arts and culture” and “the creative industries” is driven by a transactional economic mindset. Within that mindset there is an ongoing “crisis” over access, aging and declining audiences, precarity, funding, rising costs etc.

Noticeably absent from policy discourse is any detailed consideration of the cultural value of the amateur sector in and off itself, or any detailed consideration of its role and significance in the sustainability and development of the wider arts, culture and creative sector.

So I thought I’d gather some information and share it on this page to inform those conversations.

Some Numbers to Start off with

A survey was distributed in spring 2024 through the Drama League of Ireland (DLI) and the Association of Irish Musical Societies (AIMS) to their members. To date the survey has secured 110 responses, 70% of which were from Drama Groups and 30% from Musical Societies. Not all the responses answered all of the questions, presumably because some data simply wasn’t available to the respondent, so the answers had to be adjusted in some cases. This is not to suggest that the adjusted totals are correct, rather the best we can say is that the truth lies somewhere between the total and the adjusted total. The data will also require futher checking and cleaning but this is what we have so far:

| Total | Adjusted Total | |

| Number of Groups that responded | 110 | 110 |

| Average Years in Existance | 40 | 40 |

| Total Membership | 6864 | 6864 |

| Number of Shows Produced in 2023 | 141 | 246 |

| Total Number of Performances | 738 | 1,652 |

| Total Royalties Paid to Authors | €78,576 | €120,046 |

| Total Audience | 103,047 | 230,629 |

| Total Value of Ticket Sales | €1,102,045 | €5,537,002 |

But these figures are just a sample, right?

The 110 respondents are a sample – approximately 25% of the total number of Musical Societies and Drama Groups affiliated to either DLI or AIMS. Given the offiicial membership numbers of both DLI and AIMS we can speculate that the entire sector is four times the size of the adjusted numbers above, and may look something like this:

| Adjusted Totals (sample) | Projected Sector Totals | |

| Number of Shows Produced in 2023 | 246 | 984 |

| Total Number of Performances | 1,652 | 6,608 |

| Total Royalties Paid to Authors | €120,046 | €480,184 |

| Total Audience | 230,629 | 922,516 |

| Total Value of Ticket Sales | €5,537,002 | €22,148,008 |

Finding a recent number for professional theatre audiences in Ireland is challenging (but we will keep looking). We do know that in 2017 Ticketmaster sold 860,946 for “arts, theatre and comedy events”, (Irish Times, 2017) and there is no doubt that there is audience crossover between this audience and the 922,516 tickets sold for amateur events. We are of course comparing different years so its probable that the Ticketmaster number is larger for 2023. We also have to consider the anecdotal data from many arts centres about how challenging it is to cross-sell professional shows to the audience for amateur events. If this is the case then we can propose that the amateur audience constitutes a significant additional audience.

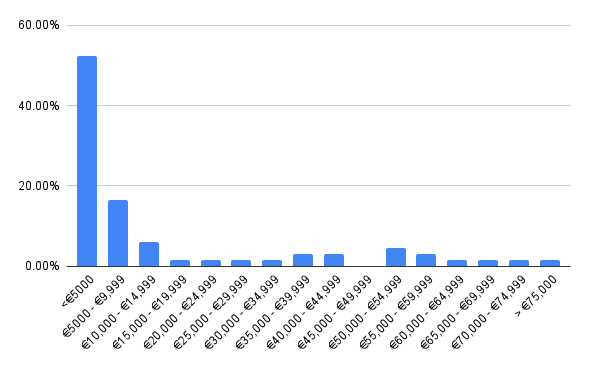

Budgets

The first thing to remember here is that 70% of the respondents are Drama Groups, and 30% Musical Societies. Musicals are more expensive than plays, so I expect that these numbers will move upwards as more data from musical societies comes in. For the moment, based on the sample we can say this about budgets:

As you can see, based on the sample data it would appear that just over 50% of the shows were produced for less than €5,000 and almost 80% were produced for less than €15,000. We can speculate that the total adjusted spend on shows in our sample is approximately €3.9million (total number of shows multiplied by average budget), which suggests that the total spend across the entire amateur sector on production is approximately €15.7 million.

Remember that production costs in many cases (but not all cases) include rent paid to professional theatres and arts centres funded by Local Authorities and the Arts Council. This is not to suggest that rent should not be paid, it is to make the point that the amateur sector constitutes a significant flow of income to those venues that constitute the professional arts infrastructure.

There is a value add of approximately €6.45 million (Total Ticket sales less the total production budget spend). Some of this will accrue to some of the societies as surplus, and some will accrue to various venues as their share of box office.

What about the people?

Very little data has been gathered about the participants and the audience, and that data is speculative: asking people in the organisation to say what they think/feel their demographic is. What we can say here is that these results indicate what certain people within the societies feel about their society and its audiences. To take one key metric – the average age:

The question here was poorly phrased, so what this means is that 55% of the respondents felt that the average age of participants in their society was somewhere between 25 and 44. There are many interesting ways to think about this, not least being that the average age of participants in the amateur sector is younger than the average audience for professional work. If this is true then a whole range of questions open up about value, participation, taste etc.

What’s equally interesting is the perception of their audiences

To put it very simply it looks like the audience is 10 years older than the participants! But again, almost 50% of the respondents put the average age of their audience somewhere between 45 and 54, and another 34% put the average age of their audience as somewhere between 35 and 44. A study of 2022 audience data commissioned by Theatre Forum Ireland (2023) seems to indicate that 50% of the audience is over 55. Again, lots of interesting questions emerge from all of this about the relative audience ages for amateur and professional work.

Conclusions

It’s impossible to draw definitive conlusions at this stage. We are working with a sample (albeit a good sized sample), however we have had to adjust numbers and speculate based on averages within the sample. What can’t be denied is that the amateur sector is a hugely significant part of the wider arts/culture/creative industries ecosystem in terms of participation, audiences, copyright payments, ticket sales and economic contribution. It’s also interesting to note that Baumol’s “cost disease” has caught up with the sector and anecdotally many societies are finding it hard to fund their work through their traditional funding models.

Its interesting to look at this through a systems thinking lens and realise that the activity in the amateur sector is creating a number of “flows” into the professional sector through copyright payments, venue rentals, box office splits, and – in the case of some societies – the contracting of professional practitioners. A good systems approach would be to look at the relationship, at the nature of the flow, and ask how might we change it to the benefit of the wider system?